Hermès The Eternal Moat

- Tung

- 5 jun

- 65 minuten om te lezen

Bijgewerkt op: 6 jun

The Business: A Saddle Maker That Never Stopped Being One Hermès was founded in 1837 by Thierry Hermès as a harness and saddlery workshop in Paris, serving the carriage trade of a city that still moved by horse. This origin is not a piece of trivia. It is the genetic code of everything the company has become. When the automobile destroyed the carriage trade, a lesser house would have died with its market. Hermès instead reasoned that its true asset was not the saddle but the capacity to work leather to the highest standard achievable by human hands, and that this capacity could be redirected toward whatever objects wealthy people wished to carry. The leather bag was, in this sense, simply the saddle's successor, the same craft, the same materials, the same obsessive standard, applied to a new object for a new century. The company has changed what it makes many times. It has never once changed what it is.

Today the company organises itself into sixteen métiers, a French word that means something closer to craft or trade than to division. This linguistic choice matters, because it signals that each business is understood internally as a discipline of making rather than a profit centre to be optimised. The undisputed core is Leather Goods and Saddlery, which encompasses the Birkin and Kelly bags around which the entire Hermès mythology orbits, along with smaller leather goods, luggage, and the equestrian products that remain, charmingly, a real business. Leather Goods accounts for somewhat more than forty five percent of group revenue and, more importantly, it is the principal engine of growth. In 2025 it expanded by thirteen percent, accelerating to nearly fifteen percent in the fourth quarter, and in the first quarter of 2026 the métier itself grew over nine percent even as the rest of the luxury sector struggled. When analysts speak of Hermès's desirability, they are very largely speaking about this one métier.

The other fifteen crafts surround and support this core. Ready to Wear and Accessories is the second largest business and has become a genuine growth driver in its own right, helped by the cultural cachet of the house's runway shows. Silk and Textiles, the scarves and ties that were, for an earlier generation, the most recognisable Hermès products, grew nearly eight percent in early 2026 and remains a high margin signature. The Watches métier, which had been a relative laggard, declined modestly through 2025 and into 2026, reflecting a broader malaise in the watch market, though the house continues to invest in it with characteristic patience, treating a soft patch as an opportunity to build rather than a reason to retreat. Perfume and Beauty, the most accessible and therefore the lowest margin entry point into the brand, was roughly flat. And the cluster the company files under Other, principally Jewellery and the Home universe, was among the faster growing adjacencies, suggesting that Hermès still has white space to colonise within its existing client base.

Geographically, the report must correct a figure that recurs in the popular bull case. It is frequently said that Asia represents around forty percent of Hermès revenue. The true figure is higher. Asia including Japan accounts for roughly half of group sales, on the order of eight billion euros against a sixteen billion total, with Greater China the single largest country exposure within that. Europe including France contributes roughly a quarter, of which France alone is about a tenth of the group. The Americas, despite being the region where the world is currently minting the most new wealth, represents only around seventeen or eighteen percent of sales. The Middle East is a smaller but rapidly growing slice. This geographic shape is the single most important fact to hold in mind for the risk discussion later, because it means two things simultaneously, that Hermès is more exposed to a Chinese slowdown than the casual bull realises, and that it is underexposed to the American boom, which is either a problem or, more plausibly, an enormous untapped runway. We will return to this.

The aspect of the business that deserves the most attention, and which receives the least in most write ups, is the manufacturing model, because it is the manufacturing model, not the marketing, that actually produces the scarcity. Hermès does not buy scarcity. It builds it, slowly, out of buildings and people. The company trains its own artisans in dedicated schools, a process that takes between eighteen months and three years before a maker is trusted to produce a finished bag alone. It owns its tanneries and has invested heavily up the supply chain to control the flow of the finest hides. And it expands its production capacity by constructing new leather goods workshops, or maroquineries, on a deliberate and public cadence. The twenty fourth such workshop opened in 2025 at L'Isle d'Espagnac in the Charente, with further sites scheduled through 2030. Each of these takes years to build and to staff, which means the company's near term production capacity, and therefore its near term revenue from its most important métier, is largely predetermined by decisions made years earlier. This is why Hermès's leather goods growth runs at a steady high single to low double digit pace rather than spiking and collapsing with demand. The binding constraint on the business is not how many Birkins the world wants. The world wants effectively infinite Birkins. The binding constraint is how many Hermès has chosen to be able to make, and it relaxes that constraint at a pace calibrated to keep desire permanently ahead of supply. The supply curve is, in effect, a policy variable.

The Addressable Market: More Rich People, And In Different Places

A mass market company is ultimately bounded by the size of the human population and by how much of its income people will spend on a given category. Hermès faces no such ceiling. Its true addressable market is the population of the genuinely wealthy, and that population is not merely growing but growing faster than at almost any point in modern economic history, while simultaneously redistributing itself across the map in ways that are quietly favourable to the house.

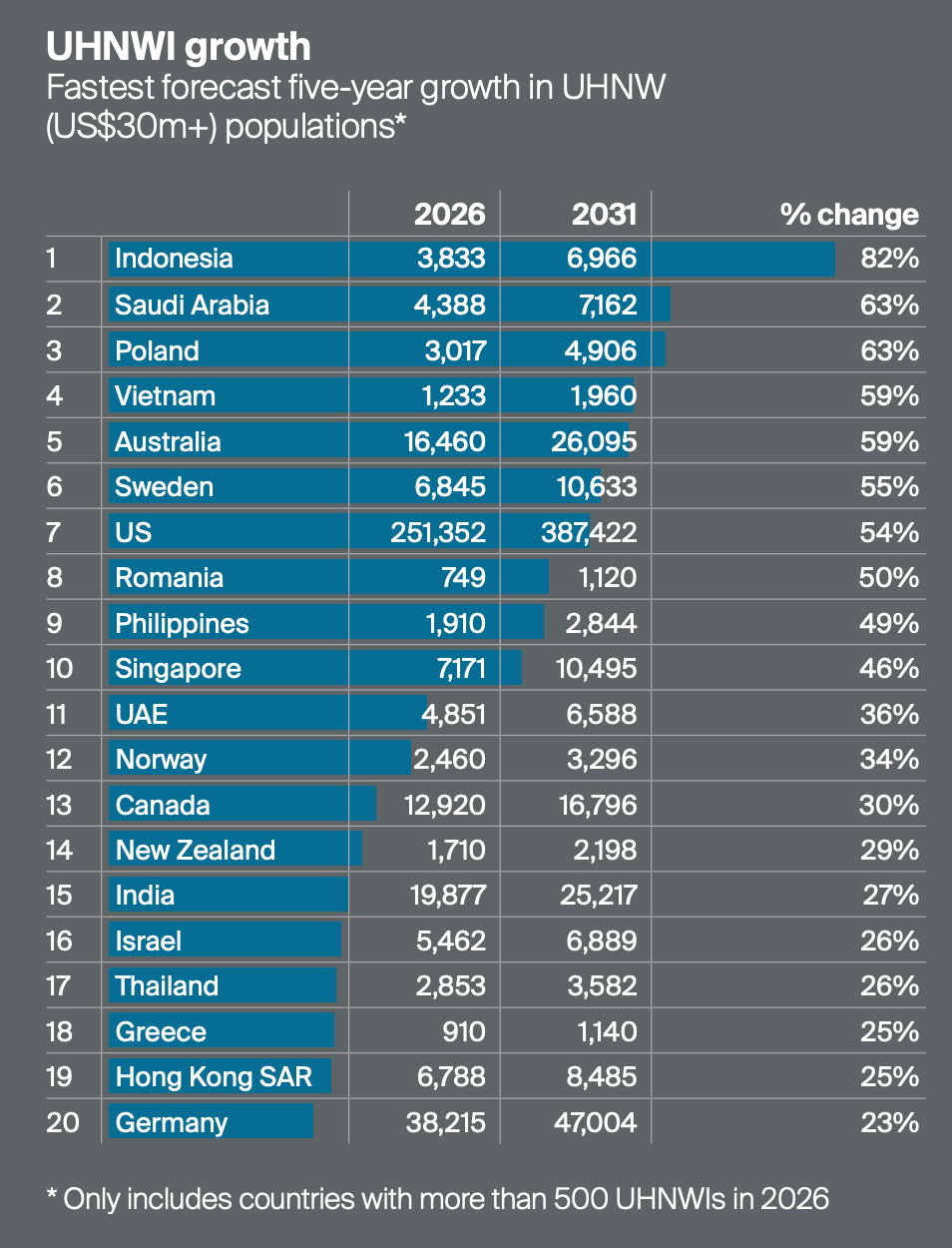

The most authoritative single source on this is Knight Frank's annual Wealth Report, whose 2026 edition documents that the global population of ultra high net worth individuals, defined as those with a net worth above thirty million dollars, rose from roughly 551,000 in 2021 to roughly 714,000 in 2026. The same model projects that this cohort will grow by a further twenty eight percent over the next five years. The billionaire count, narrower and noisier, is expected to rise roughly a quarter by 2031. Whatever one's view of the precise figures, and wealth sizing models are inherently imprecise, the direction and the order of magnitude are not seriously disputed across the major wealth research houses. The pool of people who can, without thinking about it, afford a Birkin is expanding at several times the rate of the general population.

But the more interesting story for an investor is not the aggregate growth. It is the geography of that growth, and here the data does something genuinely useful, because it reframes the China problem. The single largest engine of new ultra wealth on earth today is the United States, which accounted for roughly forty one percent of all newly minted ultra high net worth individuals over the past five years and which is forecast to push its share of the global total higher still by 2031. India has been expanding its ultra wealthy population at better than sixty percent over five years and is now the sixth largest such market in the world, with its billionaire count forecast to rise by half again by 2031. The fastest five year forecast growth rates belong to Indonesia, Saudi Arabia, Vietnam, and Poland, each in the high fifties to low eighties of percent. Europe, often dismissed as stagnant, quietly added more than thirty seven thousand ultra wealthy individuals over five years, with Germany leading the continent. The Middle East is steadily increasing its share of the global total.

The strategic implication is the spine of the entire China counter argument, so it is worth stating plainly. The geography of new wealth is shifting decisively toward markets where Hermès is underpenetrated, above all the United States, but also India and the Gulf, and away from over reliance on any single country. Hermès earns roughly half its revenue in Asia today but is creating most of the world's new customers somewhere else entirely. This is not a contradiction to be feared. It is a runway to be filled. The early evidence is already in the numbers, since in the first quarter of 2026 Hermès's sales in the Americas grew more than seventeen percent, and in Japan more than ten percent, even as Asia Pacific excluding Japan grew only modestly. A house that is structurally short the fastest growing wealth pool on earth, and that is already growing seventeen percent there, has a more durable demand outlook than one whose fortunes are chained to a single market. The China slowdown is real, and we will treat it seriously in the risk section, but the addressable market data tells us it is a cyclical headwind operating against a structural tailwind, not the structural threat the share price reaction sometimes implies.

The Moat: Six Layers, Examined To Destruction

Everything in this report ultimately reduces to one question, which is whether there is a durable reason that Hermès can charge what it charges, grow as it grows, and earn what it earns, and whether that reason will still hold in twenty or thirty years. This is the moat, and because the entire valuation premium rests upon it, we will not assert it. We will excavate it, layer by layer, and at the end we will identify the one place where it is genuinely thin.

The Anthropology of Desire: Why This Demand Is Permanent

Most competitive advantages derive their durability from some feature of the present world, a technology that is currently superior, a network that is currently the largest, a regulation that currently exists, a cost structure that competitors currently cannot match. Each of these is real, and each carries within it the seed of its own obsolescence, because the present world is precisely the thing that changes. The deepest moats are the ones rooted not in a state of the world but in a feature of human nature, because human nature is the one variable that does not change on any timescale relevant to an investor. Hermès's moat is of this rarest kind. It does not sell handbags. It sells a solution to a problem that every human society in recorded history has faced, which is the problem of how to signal one's position in a hierarchy of status, taste, and belonging in a way that others cannot cheaply imitate.

The intellectual scaffolding for this is more than a century old and rests on several distinct ideas that reinforce one another. The first is Thorstein Veblen's concept of conspicuous consumption, articulated in 1899, which observed that for certain goods, demand rises rather than falls with price, because the price is the point, the expense is what makes the object an effective signal of wealth. A Birkin is a near perfect Veblen good. Lowering its price would, paradoxically, destroy much of its value, because the high price is doing the signalling work. The second idea, drawn from evolutionary biology, is the handicap principle, formalised by Amotz Zahavi, which holds that a signal is credible precisely to the degree that it is costly and difficult to fake. A peacock's tail is honest because only a healthy peacock can afford to carry it. A Birkin is an honest signal of wealth and social position because acquiring one is genuinely difficult, expensive, and time consuming. The third is the economist Fred Hirsch's notion of positional goods, goods whose entire value derives from the fact that others do not have them, so that satisfaction is inherently scarce and cannot be manufactured by simply producing more. The fourth is Pierre Bourdieu's analysis of taste as a marker of class, in which the possession and display of certain objects functions as cultural capital, a way of asserting membership in an elite that recognises its own.

These are not academic curiosities. They are, collectively, the most durable demand function in commerce, because they describe drives that predate capitalism, predate industrialisation, predate writing itself. Archaeologists find status objects, such as rare shells, worked stone, and ornaments of materials that had to be carried over enormous distances, in the graves of societies that had no money and no markets. The impulse to signal status through the possession of the difficult to obtain is not a consumer trend that fashion invented and fashion can therefore retire. It is a constant of the species. What Hermès has done, with more discipline than any other commercial enterprise in history, is to build the most elegant and durable machine ever constructed for converting that permanent human impulse into recurring revenue and expanding margin. The genius is not in any individual bag. The genius is in having located, and patiently monetised, a feature of human psychology that will be exactly as present in 2056 as it was in 1837.

The Waiting List Is The Product

The single most misunderstood feature of Hermès, by people who do not study it closely, is the waiting list. The casual observer treats it as a supply chain failure, an embarrassing inability to make enough product to meet demand, the sort of operational deficiency that any competent management would fix. This gets the entire business backwards. The waiting list is not a failure of the system. It is the system. It is, quite possibly, the most valuable single piece of intellectual property the company owns, and it is the part of the moat that competitors have found completely impossible to replicate.

Consider what the waiting list actually does. You cannot walk into an Hermès boutique and buy a Birkin with money, no matter how much money you have. Instead you build a relationship with a sales associate over months or years. You demonstrate your taste and your commitment by purchasing across the house's other métiers, the scarves, the shoes, the homewares, the smaller leather goods, and eventually, if you have earned it, you are offered the opportunity to buy a bag. This mechanism accomplishes several things at once that a simple high price could never accomplish. It converts the acquisition of the bag from a transaction into an achievement, which deepens the emotional attachment of the buyer and ensures that satisfaction is never fully consummated. The buyer who finally receives a Birkin does not feel the deflation that follows most luxury purchases but rather a validation that immediately rekindles the desire for the next one. It filters the client base for exactly the kind of devoted, multi category, high lifetime value customer the house wants, screening out the one time speculator. And because the signal being purchased is not merely that one has money but that one has the taste, the relationships, and the patience that money alone cannot buy, it is a stronger status signal than price could ever produce, because it cannot be shortcut by a sudden influx of cash. The newly rich can buy a rival's bag the day their liquidity event clears. They cannot buy the Birkin relationship.

This is why competitors who have attempted to manufacture similar scarcity have largely failed, and the most instructive failure is Chanel's, to which we will return in detail in the competitive section. It is comparatively easy to raise prices. It is extraordinarily difficult to build, over decades, a culture of allocation in which the privilege of purchase is earned rather than bought, and in which the entire client base understands and accepts those rules. You cannot install that culture by decree, and you cannot acquire it. It must be grown, in the way that Hermès has grown it, over a very long time, and the time itself becomes a barrier to entry.

Scarcity As Strategy, Not Symptom

The waiting list is the consumer facing expression of a deeper strategic choice that runs against the logic of essentially every other business on earth. The default logic of commerce is that demand is good and more demand is better, that production should expand to meet demand, that scale lowers unit costs and raises profits, and that the job of management is to sell as much as the market will absorb. Hermès has rejected this logic for the better part of two centuries, and it is the rejection, more than anything else, that produces the financial results that astonish observers.

The company deliberately grows the supply of its most desirable products more slowly than demand grows, and it does so as a matter of explicit policy rather than operational limitation. The capacity additions are real and substantial, those two dozen and more workshops and the steady pipeline of new ones, but they are calibrated to expand output at a controlled pace that keeps the gap between desire and availability permanently open. The result is a kind of perpetual motion machine for pricing power. Because supply never catches demand, the company can raise prices every year, in good times and bad, without meaningful volume loss, because the constraint was never price in the first place. It was access. A normal company that raised prices into a downturn would watch volumes collapse. Hermès raises prices into a downturn and the only thing that happens is that the waiting list shortens slightly. This is the structural source of the pricing power that everything else flows from, and it is durable precisely because it is self imposed. A competitive advantage that depends on a rival's weakness can be erased by the rival's improvement. A competitive advantage that depends on your own refusal to maximise volume can be erased only by your own loss of discipline, which, in a company controlled by a family explicitly structured to preserve that discipline across generations, is the least likely failure mode imaginable.

The Monopoly Of Desire: The Substitution Test

The cleanest possible measure of a moat is to ask a single question about the customer at the very top of the market, which is what her next best alternative is when she wants the ultimate object in a category. The width of a moat is, in a precise sense, the distance between the first choice and the second. And it is here, on this test, that Hermès separates not only from the broad field of luxury but even from its closest structural analogue.

Take the comparison that the bull case most often reaches for, which is Ferrari, and which is genuinely apt because Ferrari shares the deep logic of Hermès, artificial scarcity, extraordinary pricing power, a brand mythology that transcends the product, and a deliberate refusal to maximise volume. Ferrari is, by almost any measure, one of the greatest businesses in the world, and we will treat it with respect in the competitive section. But apply the substitution test. A person of serious wealth who wants the ultimate statement automobile has a genuine menu. She can have a Ferrari, certainly, but she can also have a Lamborghini, a McLaren, a Bugatti, a Pagani, a Koenigsegg, or a Rolls Royce, and each of these is a credible apex object that commands its own mythology and its own devoted following. The desire Ferrari serves is real and permanent, but the supply of substitutes that can serve that same desire is plural. Ferrari competes, even at the very top, for a share of a contested wallet.

Now apply the same test to the Birkin. A woman at the apex of global wealth who desires the single most coveted leather object in the world has, functionally, one answer. She can wait for a Birkin, or she can wait for a Kelly, and the Kelly is also made by Hermès. There is no second house. Chanel is beautiful and desirable and we will discuss it at length, but the Chanel flap bag does not occupy the same psychological territory. It is a fashion object, gorgeous and storied, but it is not the apex leather craft object, and the difference is legible in the secondary market and in the cultural shorthand of every language on earth. Louis Vuitton is more accessible by design. Dior is more fashion forward and more dependent on its creative director. Bottega Veneta is the connoisseur's choice but operates at a different scale of mythology. The brutal fact, for any rival, is that the closest substitute to an Hermès Birkin is an Hermès Kelly. The company competes against itself at the top of the category, which is the definition of a monopoly of desire, and it is a competitive position of a purity that essentially does not exist elsewhere in consumer goods.

The secondary market substantiates this rather than relying on assertion, and it does so with a nuance that the honest analyst must carry, because the popular telling of the resale story is wrong in a way that matters. Hermès dominated the luxury resale market through 2025. Its core styles retained well over a hundred percent of their retail value, meaning they sold above what the buyer originally paid, in a market where essentially every other handbag depreciates the moment it leaves the boutique. At the very top, a Birkin once owned and customised by Jane Birkin herself sold at auction in 2025 for over ten million dollars, the most ever paid for a handbag, while Sotheby's alone has moved on the order of a hundred million dollars of Birkins since 2021. No other handbag behaves remotely like this. The widely repeated claim that the resale premium has compressed to around one and a half times retail is, at best, a stale blended average dragged down by the unfashionable middle of the distribution, the common full size bags that genuinely did cool and that were always the speculative end of the market. It is simply wrong for the formats that carry the mythology. Against a 2026 retail of roughly eight thousand euros for a leather Mini Kelly and roughly nine thousand six hundred euros for a Birkin 25, current secondary market floors for desirable pieces in good condition sit around twenty two to twenty four thousand euros for the Mini Kelly and nineteen to twenty thousand euros for the Birkin 25, which is roughly two and three quarter to three times retail for the one and around two times retail for the other. The asset appreciation fever of the pandemic has cooled at the speculative margin. The category of one, measured where it actually counts, has not.

The Lindy Effect: Time As An Asset That Cannot Be Bought

There is a property of certain non perishable things, formalised by Nassim Taleb under the name the Lindy Effect, which holds that for things that do not naturally decay, every additional period of survival increases the expected remaining lifespan. A technology that has lasted fifty years is likely to last another fifty. A book in print for two centuries is more likely to be read in another century than a book published last year. The logic applies with unusual force to a business whose value rests on accumulated legitimacy rather than on a current technological edge, and Hermès is the purest example in commerce.

The company has now survived for nearly a hundred and ninety years, and the list of things it has survived is itself the argument. It survived the mechanisation of transport that destroyed its original market. It survived two world wars fought across its home territory. It survived the Great Depression. It survived the rise of mass produced fast fashion, which might have been expected to render artisanal leatherwork an anachronism and instead made it more precious. It survived the digital revolution, the various luxury downturns of the past four decades, a global pandemic that shuttered its boutiques, and, most tellingly, a determined hostile takeover attempt by the most aggressive acquirer the luxury industry has ever produced. Each decade of survival is not merely evidence of resilience. It is an actual addition to the asset, because the age of the house is itself a component of its value. When an artisan stamps a finished bag with the year of its making, that stamp carries nearly two centuries of accumulated meaning, and there is no amount of capital that a new entrant could deploy to manufacture that meaning, because the only input is time, and time is the one resource that cannot be accelerated, purchased, or competed away. A rival with infinite money could build the workshops, hire the artisans, source the leather, and open the boutiques, and at the end of all that effort it would have a very good leather goods company that was zero years old. The one thing it could never buy is the years.

Technological Immunity And The Robotics Paradox

We come now to the layer of the moat that is least appreciated and that may, over a thirty year horizon, prove the most important, because it inverts the threat that hangs over almost every other great business of our era. The dominant anxiety of the present moment, for investors and for society, is technological disruption, the fear that some new paradigm will render today's leaders obsolete, as has happened repeatedly across the history of capitalism. The greatest technology businesses of our time live under exactly this shadow, however invisible it currently seems. The most fearsome moats in the market today are contingent on the continuation of a specific technological order, and over a long enough horizon, contingency compounds into genuine probability.

Hermès faces no such contingency, and here it is worth drawing the contrast explicitly, because the comparison flatters Hermès in a way that is analytically fair rather than merely rhetorical. Consider the businesses widely held to possess the strongest moats of the present era. A dominant chip design platform's advantage rests on the continued primacy of a particular computing architecture. Should a fundamentally different approach to computation achieve commercial viability over the next few decades, the moat could become a historical curiosity. A monopoly supplier of advanced lithography equipment depends on silicon remaining the substrate of computation and on a particular physical approach to etching it. Alternative materials or methods could, in principle, erode that position. These are not predictions. They are possibilities, and the point is not that they are likely but that they are conceivable, and that conceivable disruptions, accumulated over thirty years, are exactly what destroy seemingly impregnable franchises. The investor in any technology moat is, whether she likes it or not, making a bet on the persistence of a paradigm.

The investor in Hermès is making no such bet, because the proposition underlying the business is independent of any paradigm. The claim is simply that wealthy human beings, three decades from now, will still desire beautifully made objects, crafted by skilled hands from rare materials, that signal taste and status and the capacity to acquire the difficult. There is no technological development currently visible, or even plausibly imaginable, that threatens this proposition. A Birkin is not vulnerable to a better algorithm. The craft that makes it, the materials it consumes, and above all the emotional and social transaction it represents are not improved upon by any conceivable advance in computation, materials science, or automation.

And here is the inversion, which is the genuinely interesting part. The great technological wave of the coming decades, the automation of cognitive and physical labour by artificial intelligence and robotics, is, for almost every business that makes physical things, a threat or at best a cost saving. For Hermès it is a tailwind, and possibly a large one. The logic is straightforward once stated. As machines become capable of producing essentially any functional object with near perfect quality at a vanishing marginal cost, the economic and social value of objects made demonstrably by human hands does not fall. It rises, because scarcity rises. When anything useful can be produced by a machine for almost nothing, the one thing that becomes genuinely scarce, and therefore genuinely prestigious, is the irreplaceable application of human skill. A bag made over many hours by a single trained artisan, using techniques refined across generations, from materials that themselves required human expertise to select and prepare, becomes not merely a luxury but a monument to human skill at the precise historical moment when human skill is being displaced from economic production. This is not speculation. The premium attached to the visibly handmade is already observable across categories, from master forged Japanese knives to bespoke tailoring to hand thrown ceramics, and that premium has been widening, not narrowing, as automation has advanced. Hermès, which has spent nearly two centuries positioning itself as the deliberate antithesis of industrialisation, is therefore structurally long the very force that most of the economy fears. The age of the machine will make the work of the human hand more precious, and Hermès owns more of that work, at the highest standard, than any other enterprise on earth. Of all the layers of the moat, this is the one the market is least equipped to price, because it requires believing that the dominant technological story of the era will, for this one company, run in reverse.

Ownership As Armour

The final structural layer of the moat is the one that protects all the others from the single greatest threat a great business faces, which is not external competition but internal compromise, the slow erosion of discipline under the pressure to grow faster, sell more, and extract more in the short term. Hermès has fortified itself against this in a way that is essentially unique, and the story of how it did so is also one of the great corporate dramas of the century.

Beginning around 2010, Bernard Arnault, the architect of LVMH and the most formidable acquirer the luxury industry has ever known, quietly accumulated a stake in Hermès that eventually reached the high teens as a percentage of the company, building the position through financial derivatives in a manner that concealed it from the family and the market until it was suddenly revealed. It was a takeover attempt in all but name, aimed at the one trophy the conglomerate did not own. The Hermès family's response was decisive and permanent. They consolidated the great majority of the family's shares into a holding structure, built upon the historic Émile Hermès SARL and embodied today in the entity known as H51, with voting agreements that prevent any individual branch from selling out and that lock the family's control in place across generations. The effect was to render the company functionally impossible to acquire. Arnault's stake was ultimately unwound and distributed away by 2017. The episode is usually told as a thriller, and it is one, but its significance for the investor is structural. Hermès is now controlled by a family holding that owns well over half the company and is contractually bound together, led by a sixth generation family member, Axel Dumas, as executive chairman. This means the patient, supply disciplined, margin rich, anti volume strategy that produces all the financial magic is not at the mercy of activists demanding faster growth, nor of a quarterly earnings treadmill, nor of a future management tempted to flood the market with Birkins to make a number. The ownership structure is, in this sense, the meta moat. It is the thing that guarantees the company will keep doing the difficult, counterintuitive things that created the moat in the first place. Governance is not a footnote to the Hermès thesis. It is load bearing.

Where The Moat Is Actually Thin

Honesty requires identifying the one place where this otherwise overwhelming structure is genuinely vulnerable, and it is not where the bears usually look. The instinct to signal status is permanent. The specific form that the signal takes is not. Status codes rotate over time even though the underlying drive does not. There was an era when the apex female status signal was fur. There was an era, in the 1980s and 1990s, when it was the conspicuous display of logos. The present era has swung toward logo free quiet luxury, in which the signal is legible only to those who already know. Each of these was, in its day, as self evidently permanent as the Birkin feels now.

The real long term threat to Hermès, therefore, is not that a competitor will out craft it, which is close to impossible, but that the medium of apex signalling might migrate away from the leather handbag altogether, toward something else entirely, rare experiences, watches and jewellery, contemporary art, longevity and wellness, or conspicuous philanthropy. If, over thirty years, the ultimate signal of having arrived ceases to be an object one carries and becomes something one does or experiences, then Hermès's monopoly, however pure, would be a monopoly over a category that the wealthy had quietly stopped caring about most. This is the question that a pressure tested case must hold open rather than dismiss. The rebuttals are genuinely strong, and they are the reason this remains a thin vulnerability rather than a fatal one. Hermès is not a one object company. It spans sixteen métiers including the watches and jewellery toward which signalling might migrate, so it has some claim on the destination as well as the origin. More fundamentally, Hermès anchors its identity not in a particular aesthetic or a particular object but in craftsmanship itself, which travels across forms. If the apex signal moved toward a different handcrafted object, Hermès would likely be positioned to make it. And the historical record is decisive, since this is a company that has already navigated the death of the saddle, the rise and fall of the scarf as primary product, and multiple wholesale rotations of fashion, surviving each by treating its true asset as the craft rather than the object. The migration risk is real and it is the correct thing to worry about, but Hermès's answer, that it sells the human hand and not the handbag, is the most convincing answer any house in the industry could give.

The Social Media Amplifier: Does Betting On Migration Mean Betting Against Signalling?

There is a powerful objection to the migration risk that deserves its own section, because it is correct in its core and because getting the logic exactly right sharpens both the bull case and the honest statement of the risk. The objection runs as follows. We now live in a world mediated by social media, in which images, and the signalling they carry, have become more central to daily life than at any previous moment in history. This is precisely why travel has become such an obsession for the current generation, and why the open display of material success has, if anything, intensified rather than retreated. If all of that is true, then betting that the wealthy will rotate out of expensive handbags into other things is, at least in part, a bet that signalling itself is in decline. And signalling is plainly not in decline. So is the migration risk overstated?

The instinct is right, and the conclusion it points toward is largely right, but it rests on a conflation of two different things that are worth pulling apart, because once separated they tell a more precise and more useful story. There are two distinct variables at work. The first is the intensity of status signalling, how much people signal, to how large an audience, and how much they are therefore willing to spend on the objects and experiences that do the signalling. The second is the medium of status signalling, which particular objects or experiences the drive flows through at a given moment. The migration risk concerns only the second variable. It never claimed the first was in decline.

On the first variable, the objection is not merely right but emphatically so, and this strengthens the deepest pillar of the entire thesis. Social media is the most powerful amplifier of status signalling in human history. When Veblen described conspicuous consumption in 1899, the audience for a status display was the dinner party, the opera box, the people physically in the room, perhaps a few dozen at a time. The feed has replaced the dinner party with a broadcast tower available to every individual on earth. The audience for a single status signal has scaled from dozens to potentially millions, the act of signalling has become continuous rather than occasional, and the response has become quantified, in followers and likes and reach, so that signalling now carries a measurable and almost addictive return. Whatever one believes about whether this is good for human beings, it is unambiguously good for the demand function that sits underneath Hermès. The drive to signal status through the possession of the difficult to obtain is not fading in the social media era. It is compounding. The anthropology of desire that anchors this report is, if anything, accelerating, and the objection is correct that any bear who quietly assumes signalling will weaken is betting against the strongest current of the age.

But notice what this does and does not settle. Total signalling can boom while the share of it that flows through any single medium shrinks. The two move independently. This is exactly what the travel obsession demonstrates, and it is worth reading carefully, because it cuts against the bullish conclusion as much as for it. The rise of travel and experiences as the status currency of the moment is not evidence that signalling is intensifying in a way that necessarily helps handbags. It is evidence that signalling is intensifying and simultaneously migrating toward experiences. A generation that signals harder than any before it is, in part, choosing to do so through where it has been rather than through what it carries. So the honest statement of the migration risk is not a bet that signalling declines, which would indeed be foolish, but a bet that the rising tide of signalling could lift experiences, or watches, or wellness, or art, faster than it lifts the leather handbag. Those are entirely different propositions. The lazy version of the bear case, the one that imagines people simply caring less about status, is wrong. The serious version survives, but in a narrower and more demanding form.

Where this leaves Hermès specifically is, on balance, considerably more bullish than the migration section alone suggests, because within the social media signalling boom the Birkin is close to ideally positioned. Few objects on earth are as instantly legible as an Hermès bag. It is decoded by a global audience without a caption, which is precisely the property the feed rewards. It is intensely photogenic and endlessly generative of content, from the bag reveal to the question of what is carried inside it, in a way that a great many luxury objects are not. The relationship and waiting list mechanic adds a narrative layer that is itself prime material, because the story that one cannot simply buy this with money is far more compelling content than a receipt. And the acceleration of trend velocity that social media produces, in which everyone sees everything at once and micro fashions burn out within months, is a force that punishes houses built on being fashionable and rewards the one house built on being timeless. Even the spread of counterfeits and so called dupes, which social media undeniably accelerates, tends to reinforce the apex icon by broadcasting its image to billions while leaving the genuine signal, anchored in provenance and the waiting list, intact at the only level where it matters.

The one genuine residual concern, which keeps this from being a pure tailwind, is that experiences are renewable content in a way that an object is not. A new journey furnishes a new image every time, while a handbag furnishes broadly the same image repeatedly, and a medium that rewards novelty has a structural reason to favour the experiential. This is the real mechanism behind the travel boom, and it is the most credible reason that the experiential share of signalling has genuine momentum. But experiences compete largely with other discretionary spending rather than with the occasional apex purchase, the two are not mutually exclusive in a wealthy person's budget, and Hermès in any case has a foot in the experiential and quiet luxury aesthetics that the same platforms reward. The fair conclusion is that the social media era strengthens the permanence of demand decisively, demolishes the weakest form of the bear case entirely, and leaves standing only the subtler risk that the medium of signalling rotates faster than Hermès can follow, a risk against which, as the next section argues, this particular house is the best defended in the industry.

The Competitive Landscape, Examined Closely

A table of operating margins tells you who is most profitable but not why, and the why is the entire point, because it is the why that tells you whether Hermès's position is genuinely defensible or merely currently ahead. We will therefore take the principal competitors one at a time, and for each we will ask the same questions, who is its customer, how is it positioned, why is it structurally different from Hermès, where is it superior and where inferior, and what has its growth record actually been. The cumulative picture that emerges is the real test of the category of one claim.

Chanel: The Closest Rival, And The Most Instructive

If one is forced to name a single house that competes with Hermès in the highest tier of women's luxury, it is Chanel, and the comparison is worth dwelling on at length precisely because Chanel is close enough to illuminate, by contrast, exactly what makes Hermès different. Chanel's customer is, like Hermès's, a woman of real wealth, but the nature of the desire the two houses serve is not the same, and that difference is the whole story. Chanel sells fashion, fragrance, and an idea of Parisian femininity crystallised by Gabrielle Chanel and elaborated by a century of creative directors. Its mythology is bound up with the little black dress, the No. 5 perfume, the tweed suit, and the quilted flap bag. Hermès sells craftsmanship, and its mythology is bound up with the workshop, the artisan, and the leather. The Chanel customer buys into a look and a name. The Hermès customer buys into a making. This is not a value judgement, since Chanel is one of the most powerful brands ever built, but it is a structural distinction with financial consequences.

The most revealing episode in the recent history of the two houses is what happened when Chanel attempted, deliberately, to migrate toward Hermès's positioning. Over the three years from 2020 to 2023, Chanel raised the price of its classic handbags more aggressively than any other major luxury house, by roughly sixty percent, on some analyses the steepest increases in the industry, in an explicit strategy to elevate the flap bag toward Birkin adjacent status and to capture the pricing power that Hermès enjoys. The strategy worked for as long as the luxury cycle was booming and aspirational buyers were willing to stretch. Then the cycle turned, and the difference between manufactured scarcity and genuine scarcity became starkly visible in the financial statements. In 2024, Chanel's revenue fell by more than four percent to about eighteen and a half billion dollars, its first contraction since the pandemic, and its operating profit collapsed by thirty percent to around four and a half billion dollars, down from over six billion the year before. Its Asian sales, which represented roughly half its business, fell over seven percent as Chinese demand weakened. In the very same period, Hermès grew its revenue by nearly fifteen percent and held its operating margin at forty one percent. Two houses, both heavily exposed to the same Chinese slowdown, both selling to wealthy women, and one of them grew through the downturn while the other's profits fell by a third.

The reason is precisely the difference this report has been building toward. Chanel raised prices without possessing the waiting list mechanism, without the allocation culture gated by relationship, and without the genuine leather craft heritage that justifies a Birkin's price in the buyer's own mind. When you raise prices on an aspirational fashion object that a stretched buyer can choose to forgo, and the buyer's confidence then wavers, she forgoes it, and your volumes and profits fall. When you raise prices on an object that the buyer has waited years and cultivated a relationship to be permitted to purchase, and which she believes, with secondary market evidence to support her, to be an appreciating asset, she does not forgo it, and your revenue grows. Chanel's painful 2024 was, in effect, a controlled experiment that demonstrated the value of everything Hermès has and Chanel does not. To its credit, Chanel responded not by panicking but by investing through the downturn, raising capital expenditure by more than forty percent and committing to its long term brand health, which is the correct response and reflects the patient instincts of its owners, but the episode revealed the ceiling on positioning led by price when it is not underpinned by genuine structural scarcity.

There is one further point about Chanel that is decisive for an investor specifically, as opposed to an admirer of brands, which is that it is privately held and unavailable. Chanel is owned by the Wertheimer family, the brothers Alain and Gérard, through a structure overseen by their family office, and it is not listed on any exchange. The family extracted a dividend of nearly six billion dollars from the 2023 results and has taken out well over ten billion across three strong years, which tells you both that the business is extraordinarily cash generative and that the owners have no need or intention of sharing it with the public. One can admire Chanel, but one cannot buy it, and so for the purposes of capital allocation it functions as a reminder of what the apex of the category looks like rather than as an alternative to Hermès. The practical conclusion is striking. Of the two houses that genuinely occupy the summit of women's luxury, one is structurally inferior to Hermès in exactly the ways that produce durable pricing power, and the other, which is the same one, is also impossible to own. Hermès is, for the public market investor, not merely the best option at the apex. It is very nearly the only option.

LVMH: Width Versus Depth

LVMH is the largest luxury enterprise in the world, with revenue in the range of eighty billion euros, and it is the work of Bernard Arnault, who has a serious claim to being the most consequential business builder the luxury industry has ever seen. The case for owning LVMH is real, and it is a fundamentally different proposition from Hermès, and on a long horizon the differences are what matter. LVMH's customer is everyone who buys luxury, across an enormous range of price points and categories, because LVMH owns something like seventy five houses spanning wines and spirits, fashion and leather goods, perfumes and cosmetics, watches and jewellery, and selective retail through Sephora and the travel retail channel. Its moat is width. The diversification provides genuine resilience, since when one house stumbles, others carry the group, and it provides Arnault with an unmatched machine for acquiring, reviving, and scaling brands.

But width is also dilution, and this is where the contrast with Hermès sharpens. A portfolio of seventy five houses necessarily contains brands at every stage of the luxury lifecycle, from rising stars to mature cash cows to houses in quiet structural decline, and managing creative transitions across dozens of them simultaneously is an execution challenge of staggering complexity that no amount of managerial genius fully eliminates. The group's overall operating margin, in the low twenties of percent, is excellent by any normal standard but roughly half of Hermès's, and a fair analyst must immediately add an important caveat that the casual bull case omits. The relevant comparable is not LVMH's group margin, which is dragged down by lower margin businesses such as wines, spirits, and Sephora, but the margin of its Fashion and Leather Goods division, which is the part that actually competes with Hermès and which runs in the mid thirties of percent. Measured properly, Hermès's profitability advantage over LVMH's relevant division is on the order of seven percentage points, not the twenty and more that an unfair group level comparison implies. That is still a meaningful and durable advantage, but precision matters, and overstating the gap weakens rather than strengthens the case.

LVMH's deeper issue, and the one most relevant to a thirty year holder, is succession. Bernard Arnault is in his late seventies. He has positioned five children across the group in senior roles, which is sensible planning, but a conglomerate of this complexity ultimately run by a family committee after the departure of its singular architect is genuinely uncertain territory, in a way that Hermès's succession simply is not, because Hermès has already navigated its critical ownership transition and has institutionalised its strategy across generations rather than vesting it in one visionary. LVMH's recent growth has also stalled, with its fashion and leather division declining in 2024 and 2025 amid the sector wide slowdown and its heavier exposure to aspirational and entry level buyers, which is precisely the cohort that retrenches first in a downturn. The honest summary is that LVMH is a very good business, more diversified and considerably cheaper than Hermès, with real near term cyclical recovery optionality, but it is structurally a different and lower quality animal, wider, more cyclical, more dependent on the aspirational consumer, more exposed to execution risk across its sprawling portfolio, and facing a genuine succession question. On a thirty year view, LVMH is good and Hermès is unique.

Richemont: The Jeweller's Path

Richemont is the third of the great European luxury groups, and it competes with Hermès only obliquely, which is itself informative. Its crown jewels are precisely that, jewellery and watch houses, above all Cartier and Van Cleef and Arpels, which sit at the apex of hard luxury much as Hermès sits at the apex of leather. Richemont's customer overlaps with Hermès's at the top end, and its best businesses share some of the same desirable characteristics. Cartier in particular possesses genuine heritage, real pricing power, and a mythology that transcends any individual product, and the jewellery category has held up notably better than fashion through the recent downturn because high jewellery is bought by the genuinely wealthy rather than the aspirational. Richemont's revenue is in the low twenties of billions of euros with an operating margin around twenty percent, and the jewellery houses within it are arguably as close to Hermès like quality as anything outside Hermès itself.

The reason Richemont is not Hermès comes down to portfolio quality and category economics. Alongside its superb jewellery houses, Richemont carries a collection of specialist watch brands of varying health, a watch market that has been structurally challenged, and the historical baggage of a costly and ultimately unsuccessful adventure in online luxury retail. The group is a mixture of the genuinely exceptional and the merely adequate, in a way that Hermès, with its uniform standard across every métier, is not. For an investor who wants exposure to the apex of jewellery specifically, which has its own durable, status driven, China exposed demand function, Richemont, and Cartier within it, is a serious and underrated proposition. But it is a play on a different category with a more mixed portfolio, not a substitute for the singular focus and uniform excellence of Hermès.

Ferrari: The Honest Analogue With One Fatal Difference

Ferrari deserves the most respect of any company in this section, because it is the most intellectually honest comparison to Hermès and shares its deepest logic more completely than any other business. Ferrari produces roughly fourteen thousand cars a year and has committed publicly to never expanding production beyond the level that keeps its waiting lists intact, the exact same deliberate refusal to maximise volume that defines Hermès. Its customer is the genuinely wealthy enthusiast and collector. Its pricing power is extraordinary, with average selling prices in the high hundreds of thousands of euros. Its operating margin, in the high twenties to around thirty percent, is the best in the entire automotive industry and bears comparison with the very top of luxury. Its brand mythology, built on seventy seven years of Formula One and a culture of scarcity and exclusivity, transcends the product entirely. And its capital discipline, including a substantial and growing buyback programme, is exemplary. Ferrari has proven, more convincingly than any other modern company, that the Hermès model of scarcity driven luxury works spectacularly outside of fashion. Its revenue has compounded steadily at roughly ten percent since its listing in 2015, its returns on capital are exceptional, and it has extended its brand into merchandise, lifestyle, and experiences without diluting the core.

But Ferrari carries one risk that Hermès does not, and it is potentially existential rather than cyclical, and in the months before this report was written it stopped being hypothetical and began, visibly, to materialise. The internal combustion engine is the sensory core of the Ferrari experience. The sound, the vibration, the mechanical drama of a high performance engine at full extension are inseparable from what the customer is actually buying. The transition to electric propulsion, which the wider world is imposing on the automobile, strikes directly at this core, and Ferrari has now had to confront it in the most public way possible. The company unveiled the full design of its first fully electric car, the Luce, in Rome on the twenty fifth of May 2026, a four door, five seat sedan priced at around five hundred and fifty thousand euros, developed with the involvement of the former Apple design chief Jony Ive and engineered to amplify the vibrations of its electric powertrain into a synthetic roar precisely because the natural drama of the combustion engine is the one thing it cannot reproduce. That last detail is the whole risk in miniature, since the car must manufacture an artificial version of the very quality that defined the brand.

The reception was, to put it gently, not what Maranello had hoped for. The design polarised critics and drew open ridicule, with reviewers calling its proportions crude and unbecoming of the marque and likening its silhouette to mass market electric sedans, and Luca di Montezemolo, the man who ran Ferrari through its golden era and oversaw the F40, the Enzo, and the LaFerrari, went so far as to suggest the company strip the prancing horse badge from the car before it shipped. The market reacted in kind. Ferrari shares fell about six percent by the close of the session after the reveal, with an intraday loss approaching eight percent, and this followed an even sharper reaction in October 2025, when the first presentation of the electric strategy and a more cautious long term growth plan triggered the stock's worst single session since its listing in 2016, a fall of roughly fifteen percent. None of this proves the electric Ferrari will fail. The brand's mythology is deep, deliveries have not yet begun, the Luce opens a genuinely new segment of family buyers, and a polarising design can still sell out to collectors who value rarity over consensus beauty. But it is direct, real world evidence of exactly the paradigm level risk that matters on a thirty year horizon, the genuine and now demonstrated uncertainty over whether an electric Ferrari preserves or quietly diminishes the thing that made a Ferrari a Ferrari, and the market has now priced a piece of that uncertainty in public.

A Birkin faces no equivalent question. There is no technological transition looming over the leather handbag, no regulatory force compelling its reinvention, no risk that the object of 2056 will be philosophically different from the object of today, and certainly no prospect of Hermès ever having to synthesise an artificial substitute for the very quality that defines it. This is the precise sense in which Hermès is superior even to its finest structural analogue. Ferrari shares almost every virtue of the Hermès model, and has just reminded the market, in the most public way imaginable, of the one technological vulnerability that Hermès simply does not have.

Kering And The Cautionary Tale Of Gucci

Kering is the indispensable cautionary tale of the sector, and including it is essential because it demonstrates, in real time and with real money, what happens to a luxury house that lacks the structural protections this report has been cataloguing. Kering's principal asset is Gucci, a house that rode a spectacular boom led by creativity through the late 2010s under a particular creative director and aesthetic, reached the heights of fashion desirability, and then, when fashion's restless attention moved on, as it always does, fell hard. Kering's revenue declined by roughly fifteen percent in 2025, dragged down by a Gucci collapse on the order of twenty percent, and the group has been forced into a wholesale creative and managerial reset. The lesson is the inverse of the Hermès lesson. A house whose desirability depends on being fashionable, on the current aesthetic moment, on the genius of the current creative director, on the cycling tastes of consumers driven by trends, is structurally fragile, because fashion is by definition the thing that changes, and a brand built on it is therefore building on sand. Hermès's deliberate refusal to be ahead of fashion, its insistence on timeless craft over seasonal reinvention, looks unexciting in a boom and looks like genius in a bust. Kering is what Hermès would be if Hermès had built its moat out of creativity rather than craft, and 2025 showed exactly how that ends.

The Quiet Luxury Cohort: Cucinelli, Loro Piana, The Row, And The Real Frontier

The most genuinely interesting competitive development for Hermès is not coming from the established giants but from a cluster of houses at the quiet luxury frontier, because they are competing for the same thing Hermès increasingly represents, understated, logo free luxury led by craft for people who no longer wish to signal loudly. Brunello Cucinelli is the publicly traded exemplar and the one most often mentioned in the same breath as Hermès by investors who prize quality compounders. Its customer is the discreet ultra wealthy who want the finest cashmere and tailoring without a visible logo. Its revenue, though far smaller than Hermès at a little over a billion euros, has compounded at a low double digit rate with remarkable consistency, and crucially it has continued to guide for double digit growth even as the rest of the sector stalled, which is why it has retained the affection of analysts focused on quality and a premium valuation of its own. Cucinelli is not a threat to Hermès in any direct sense, since it is a different category at a different scale, but it is proof that the model of quiet luxury, led by craft and resilient to China, commands a structural premium, which is corroboration of the Hermès thesis rather than a challenge to it.

The more pointed signal comes from The Row, the house built by the Olsen sisters, which achieved genuine unicorn status in the resale market in 2025 with retention rates rivalling Hermès itself, and which has become the brand that fashion's most discerning customers name when they want the new apex of quiet taste. The Row is tiny relative to Hermès and poses no near term financial threat, but it is worth watching closely for precisely the reason identified in the discussion of the moat's vulnerability, that it is the clearest evidence that the form of apex signalling can shift, and that a new house can, occasionally, capture the connoisseur's imagination at the very top. It is a pin prick, not a breach, and Hermès's leather monopoly is untouched by it. But the analyst who wants to know where the one real long term threat to Hermès would come from should keep an eye on the quiet luxury frontier rather than on the established giants, because if apex desire ever migrates, it will migrate there first.

What The Competitive Survey Establishes

Stepping back from the individual profiles, the cumulative picture is the actual test of the category of one claim, and it largely vindicates it while refining it. At the very apex of women's leather goods, Hermès has no genuine substitute that is also available to a public investor. Its one true peer, Chanel, is structurally weaker in exactly the dimensions that produce durable pricing power, and is in any case unbuyable. Its finest structural analogue, Ferrari, matches it on the scarcity model but carries a technological risk Hermès lacks. The diversified giant, LVMH, is wider, cheaper, more cyclical, and lower quality, with a looming succession question. The jewellery champion, Richemont, plays a different and more mixed game. The fashion led house, Kering, is the live demonstration of what Hermès has protected itself against. And the quiet luxury cohort is corroboration of the model and the place to watch for the one real long term threat. The category of one is not marketing mythology. It is, for the apex leather buyer and for the public investor simultaneously, very nearly the literal truth, and that dual scarcity, the scarcity of the product and the scarcity of the investable vehicle, is itself part of what supports the valuation premium we must now confront.

The Financials

The remarkable thing about Hermès's financial statements is how thoroughly they corroborate the qualitative story, because a moat that is real should show up as durable, expanding profitability and high returns on capital, and Hermès's do exactly that. Over the past decade the company has compounded its revenue at roughly thirteen percent annually and its net income at roughly seventeen percent, a record of consistency that embarrasses most technology companies and that has been achieved, remarkably, while raising prices every year and deliberately refusing to maximise volume, the two things that ordinary economic intuition says should be in tension with growth. In 2025 the company crossed sixteen billion euros of revenue for the first time, growing nine percent at constant exchange rates even as the broad luxury sector contracted, and it did so on the back of thirteen percent growth in its core leather métier. The trajectory of the recent past makes the compounding vivid, with revenue around nine billion euros in 2021, eleven and a half in 2022, thirteen and a half in 2023, just over fifteen in 2024, and sixteen in 2025, very nearly a doubling in four years, achieved with no acquisitions and no financial engineering, purely by making and selling more of what it has always made, at ever higher prices, to an ever larger pool of the wealthy.

The profitability is where the moat becomes legible in numbers. Hermès earned a recurring operating margin of forty one percent in 2025 on a gross margin above seventy one percent, and it has held that operating margin in the range of forty to forty two percent for years. To appreciate how extraordinary this is, one need only place it beside the field. Ferrari, the best in the automotive world, earns under thirty percent. LVMH's relevant fashion and leather division earns in the mid thirties and the group as a whole in the low twenties. Richemont earns around twenty. And most luxury fashion houses consider fifteen percent a strong result. Hermès's margin is not the product of cost cutting or financial cleverness. It is structural, the direct arithmetic consequence of pricing products at large multiples of their production cost and having customers who believe, often correctly given the resale data, that the price is justified or even too low. The one wrinkle worth noting for accuracy is that reported 2025 net profit of about four and a half billion euros was actually down slightly on the prior year, but this reflects a single French corporate surtax of roughly three hundred and thirty million euros. Excluding that one time fiscal hit, net profit would have risen about five and a half percent in line with sales, and underlying earnings power was undiminished.

The balance sheet and cash generation complete the picture and are, if anything, even more impressive than the income statement. Hermès is effectively free of debt and sits on a net cash position of nearly thirteen billion euros, with a current ratio around five and a debt to equity ratio of barely above a tenth. Its return on equity is around twenty five percent and its return on invested capital is in the region of fifty percent, figures that are almost unheard of at this scale and that reflect the capital light nature of a business whose primary input is trained human craft rather than the billions of perpetual capital expenditure that a chip equipment maker or a cloud infrastructure business must commit merely to stand still. The company converts its profits into free cash flow at among the highest rates of any large cap business in the world, generating nearly four billion euros of adjusted free cash flow in 2025 against modest capital expenditure of a little over a billion, most of which went into stores and the workshop expansion that funds future growth.

This torrent of cash raises the one genuine question about Hermès's financial management, which concerns capital allocation. Hermès is a compounder that pays dividends and reinvests rather than a buyback machine. It raised its 2025 dividend by more than twelve percent to eighteen euros a share, distributed nearly three billion euros to shareholders, and shares the fruits generously with employees through profit sharing and bonuses, but it conducts essentially no buybacks of consequence. The consequence is that cash accumulates on the balance sheet faster than it is returned or deployed, and the war chest now approaches thirteen billion euros. A purist might call this less than optimal capital allocation, idle cash earning a low return that could be returned to owners. The more sympathetic and, in this case, more accurate reading is that the cash is the financial expression of the same conservatism that runs through the whole enterprise, the cushion that lets the company remain utterly indifferent to downturns, fund its workshop expansion across many decades without ever straining, and retain the optionality to act decisively if it ever chose to. The market arguably under credits the value of that optionality and that indestructibility, but it is fair to note that a more aggressive return of capital would likely raise the stock's returns at the margin without harming the business at all.

Valuation, or why the numbers are not where the money is made

Everything to this point has argued that Hermès is an extraordinary business with the most durable moat in consumer goods. None of it, by itself, answers the only question that determines an investor's return, which is not whether this is a great business but whether it will do better than the market already expects. Those are completely different questions, and conflating them is the most common error in quality compounder investing.

Here is the uncomfortable starting point. Every number a bull recites, the forty one percent operating margin, the roughly fifty percent return on invested capital, the near thirteen billion euros of net cash, the decade of thirteen percent revenue and seventeen percent earnings growth, is public, audited, and known to every participant in the market. None of it is secret, none of it is insight, and all of it is already in the sixteen hundred euro share price. An edge cannot come from knowing these facts better, because nobody knows them worse. The market is efficient with respect to the published record.

This is why the discounted cash flow exercise, which the bull case usually treats as the centrepiece, is close to useless as a decision tool, and it is worth being blunt about why. A discounted cash flow on Hermès does not discover a value, it launders an assumption. Take the roughly four billion euros of 2025 free cash flow, grow it at ten percent for five years, fade it to six percent, set a terminal rate of three and a half percent, all generous, and the entire answer swings on the discount rate. At eight percent you get roughly thirteen hundred and fifty euros and the stock looks twenty percent overvalued. At seven and a half percent you get roughly sixteen hundred euros and it looks fairly valued. At seven percent with terminal growth lifted to four percent you get near nineteen hundred euros and it looks cheap. The model is not telling you what Hermès is worth. It is telling you what you already believed about Hermès's riskiness, dressed up as arithmetic. Whoever picks the discount rate has already picked the answer.

So the discounted cash flow is demoted here to exactly what it is, a way of reading the market's implied assumption rather than forming our own. Read that way it says something genuinely useful. At sixteen hundred euros the market is pricing Hermès with an implied discount rate of roughly seven to seven and a half percent, which is to say it is pricing one of the lowest risk equity cash flow streams in the world, closer to a high grade bond than to a stock. The bull and bear debate is entirely this single number. Both sides agree on the business. The bull says that certainty this rare deserves a near riskless rate. The bear says no equity does, that the right rate is closer to eight percent, and that any drift back toward normal re-rates the stock down twenty five to thirty five percent even if the company is flawless. That is the whole argument, and no amount of staring at the balance sheet resolves it, because the balance sheet is not in dispute.

If the facts are priced in and the discounted cash flow only echoes back your own assumption, then outperformance has to come from somewhere else. It has to come from a view about the future that diverges from consensus, and from behaviour by other market participants that you can anticipate. That is the thin line between investing and speculation, and it is the only place alpha lives. The rest of this section is built there.

The actual bet: A demand and supply gap that widens faster than consensus assumes

Outperformance requires the company to beat consensus, not merely to be good. So the thesis must rest on a variable where our expectation differs from the market's. The moat is not that variable. The moat is what guarantees the company stays relevant and protected, which secures the downside but does not, on its own, generate a surprise. The moat is the insurance, not the edge.

The edge is a specific claim about the future. It is that the gap between the number of people who can effortlessly afford the apex product and the number of apex products Hermès chooses to release is wide, and widening, by more than the market is extrapolating. Two forces drive it.

The first is the buyer pool. The global population of ultra high net worth individuals rose from roughly five hundred and fifty one thousand in 2021 to roughly seven hundred and fourteen thousand in 2026, and is forecast to grow another twenty eight percent over five years, with the fastest creation of new wealth in exactly the markets where Hermès is underpenetrated, the United States above all, then India and the Gulf. Hermès earns roughly half its revenue in Asia today but is minting most of its future customers elsewhere. The Americas already grew seventeen percent in the first quarter of 2026.

The second force is the mechanism the casual bull gets wrong. That demand does not convert one for one into revenue, because Hermès caps supply on a pre committed workshop cadence, with new sites scheduled through 2030. So the demand surge expresses itself through two channels, and it matters which one the bet rides on. Volume is largely policy determined and therefore largely knowable, since consensus can read the same workshop schedule. The real lever is price. A widening excess demand gap gives Hermès the standing right to raise prices every year, in booms and in busts, without losing volume. The consensus error we are betting against is not that they will sell more bags. It is that consensus models pricing power fading toward inflation plus a little, when the structural widening of the gap means it persists at a high single digit clip for far longer.

There is a subtlety worth stating rather than hiding. Hermès does not hold supply perfectly rigid. It allocates flexible capacity toward the hottest formats, and Mini Kelly unit sales rose sixteen percent in 2025 and twenty five percent versus 2023. So part of the upside is volume on the most wanted pieces, not only price. The mechanism is to harvest the gap intelligently rather than to freeze output. This is a strength, but it carries one implication for the kill criteria below, so it is flagged here rather than buried.

The free option: Handcraft in the age of the machine

There is a second, longer dated bet folded in at no extra cost. As automation and artificial intelligence drive the marginal cost of producing functional objects toward zero, the social and economic value of objects demonstrably made by human hands should rise, because scarcity rises. Hermès owns more of the highest standard human craft output than any enterprise on earth, which means the dominant technological anxiety of the era runs, for this one company, in reverse.

This belongs in the thesis precisely because it is almost impossible to model, which means consensus underweights or ignores it, and that is exactly where un-priced edge hides. But two disciplines apply. It is a fifteen to thirty year payoff, so it cannot justify a near term entry, since it improves terminal value rather than the next five years. And it carries a reflexive risk the simple version misses, which is that if artificial intelligence also makes counterfeits cheap and convincing, the signal could erode from the bottom even as genuine craft grows scarcer at the top. The defence, that the genuine signal is anchored in provenance and the waiting list relationship rather than in the object's appearance, so that fakes broadcast the icon without diluting it, is strong but not free. Treat this layer as a long dated call option rather than a pillar.

Where the alpha actually is: Game theory on a historic drawdown

If the facts are priced in, the entry has to be a bet on other participants' behaviour rather than on a fair value calculation. The setup right now is rare. This is among the largest drawdowns in the company's public history, roughly forty five percent from the peak, comparable in depth only to the financial crisis and the pandemic, and it has occurred while the business kept growing and while the broad luxury sector fell harder. The stock has broken its two hundred week moving average, a line it respected for years.

The game theoretic question is who is selling at sixteen hundred euros, and whether they are likely to be right. The marginal seller is almost certainly a stack of mostly price insensitive flows, with a minority of informed money. The first group is momentum and systematic funds, selling mechanically on the two hundred week moving average break. They hold no view on Birkin demand, they follow a signal, and they are price insensitive, which is our edge. The second is relative performance refugees, long only managers bleeding against an index dominated by artificial intelligence and megacap technology names, dumping a luxury laggard to chase the trade that is working. That is career risk selling rather than conviction, and it is again our edge. The third is basket level China reducers, selling Hermès as an Asia luxury proxy alongside LVMH and Kering, which is to say selling the category and ignoring that Hermès is the category of one that grew while the others shrank. This is the cleanest mispricing of the three, and the tell is simple, because if Hermès falls together with Kering and LVMH despite outgrowing them, then the market is pricing the sector and not the company. The fourth group is the one informed cohort, the multiple compression players who are explicitly betting that the de-rating from forty times toward thirty times is not finished. They are not wrong that the multiple is the risk. They simply have a shorter horizon and a higher discount rate, and the difference between them and us is not the facts but whether one is willing to own the business through the de-rating.

The honest steelman of the seller is that last group generalised, the claim that the rate regime has structurally changed and that every long duration compounder now permanently deserves a higher discount rate. This is unanswerable in advance. The only sound response is to refuse to need an answer, to assume the multiple may sit at thirty times rather than forty, to take the return from earnings rather than from re-rating, and to stage the entry so that further compression is something one buys rather than suffers.

What would break the thesis: specific tripwires, watched in pairs

A game theory position is only honest if it can be falsified. The discipline is cyclical versus structural, where cyclical weakness is a reason to buy and structural change is a reason to abandon. On every current metric the drawdown is cyclical, whether China softness, currency drag, a Middle East hit, an aspirational buyer retreat, or a soft watch market, each of which has precedent in past retraces and none of which breaks the bet. The thesis is not that nothing is wrong. It is that nothing structural is wrong, and there are specific tripwires that would prove otherwise.