Hermès The Eternal Moat

- Tung

- 15 uur geleden

- 13 minuten om te lezen

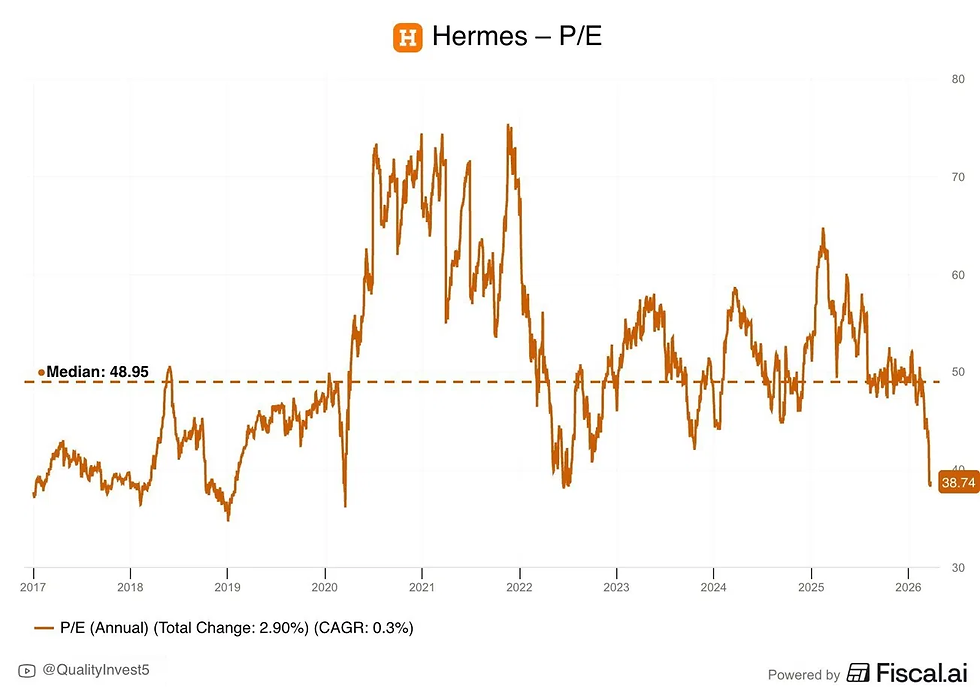

Hermès has existed since 1837, has never changed what it fundamentally does, has raised prices every year without exception, makes customers wait years to buy its most coveted products, and in doing so has compounded shareholder wealth at a rate that embarrasses most technology companies. This essay makes the case that at a current P/E of 38.7 against a ten year median of 48.95, Hermès represents one of the rare moments when the world's most durable business trades at a meaningful discount to its own history.

What an Economic Moat Actually Means

Warren Buffett popularised the concept of the economic moat to describe a business with durable competitive advantages that protect it from rivals over long periods of time. Most moats are technological, regulatory, or network based. They are real, but they carry the seeds of their own obsolescence. Technology moats erode when paradigms shift. Network moats weaken when better networks emerge. Regulatory moats dissolve when laws change.

Hermès has none of these moats. It has something far older and far more durable: it has captured a permanent dimension of human psychology. The desire for things that cannot be easily obtained, that signal mastery and taste, that are made by human hands with decades of skill, is not a trend. It is anthropology. It predates capitalism, predates industrialisation, predates writing. Hermès has simply found the most elegant commercial expression of that desire in the history of business.

Scarcity as Strategy

Most companies treat scarcity as a problem to be solved. More demand means more production, more production means more revenue, more revenue means more profit. This is the logic of virtually every business on earth. Hermès has deliberately rejected this logic for nearly two centuries.

Leather goods supply grows at roughly 7 to 10 percent annually, a rate that is deliberately calibrated to be below demand. The Birkin and Kelly bags are not available for purchase in any conventional sense. You cannot walk into a Hermès store and buy one. You build a relationship with a sales associate over months or years, you demonstrate taste and commitment by purchasing across other categories, and eventually you are offered the opportunity to buy. The waiting list is not a supply chain failure. It is the product.

This mechanism creates something extraordinary in consumer markets: a product where desire is never fully satisfied and therefore never fully extinguished. A customer who finally acquires a Birkin does not experience the deflation of purchase that afflicts most luxury consumption. They experience validation of a long pursuit, which deepens loyalty rather than completing it. They immediately begin wanting the next one.

The Lindy Effect and 187 Years of Evidence

The Lindy Effect, formalised by Nassim Nicholas Taleb, holds that for non-perishable things, every additional period of survival increases the expected future lifespan. A book that has been in print for two hundred years is more likely to still be read in fifty years than a book published last decade. The same logic applies to businesses whose value rests on timeless human needs rather than technological cycles.

Hermès was founded in 1837 as a harness workshop. It survived the mechanisation of transport, two world wars, the Great Depression, the rise of fast fashion, the digital revolution, multiple luxury downturns, a global pandemic, and a hostile takeover attempt by the world's most aggressive luxury conglomerate. Each decade of survival does not merely prove resilience. It compounds the brand's mythological status. The age of the house is itself a competitive advantage that no new entrant can purchase or replicate.

When a Hermès artisan stamps a bag with the year of its creation, they are stamping it with 187 years of accumulated legitimacy. No amount of marketing spend can buy that. No technology can manufacture it. Time is the only input, and time cannot be accelerated.

Reading the P/E History

The chart tells a clear story. Over the past decade, Hermès has traded at a median P/E of approximately 48.95. The range has been wide: compressing to around 33 during the 2019 period of uncertainty, spiking above 70 during the post-pandemic luxury euphoria of 2021 and 2022, and now sitting at 38.7 as of May 2026. That current reading places it among the cheapest entry points in its modern public history.

The compression in P/E has occurred not because the business has deteriorated but because the stock corrected from genuinely excessive valuations in 2021 to 2022 and because the near term growth narrative has softened. Q1 2026 revenue declined approximately 1 percent, Asia ex-Japan grew only 2 percent, and China caution has weighed on sentiment. These are real headwinds. They are not structural threats.

The critical distinction in long term investing is between a problem with the business model and a problem with the current environment. Hermès in 2026 faces an environmental problem: a temporarily cautious Chinese consumer, a strong euro creating translation headwinds, and a global wealthy class that is more selective after years of post-pandemic excess. None of these factors change the underlying equation that the number of people globally who can afford a Birkin will roughly double over the next thirty years, and the supply of Birkins will grow at 7 to 10 percent annually.

The Earnings Quality Argument

One of the most underappreciated aspects of Hermès as an investment is the quality of its earnings. A 41 percent operating margin is extraordinary in any context. In consumer goods it is essentially unprecedented. For comparison, LVMH operates at approximately 17 percent, Ferrari at around 27 percent, and most luxury fashion houses consider a 15 percent margin a strong result.

These margins are not the result of financial engineering or cost cutting. They are structural. Hermès prices its products at multiples of production cost not because it can temporarily get away with it but because customers believe the price is justified and in many cases insufficient. Secondhand Birkins regularly trade above retail. The asset appreciation argument for Hermès ownership is not marketing: it is empirically verifiable in auction data over decades.

The capital light nature of the model amplifies this further. Unlike ASML which must spend billions on next generation lithography research, unlike NVIDIA which must continuously outspend competitors on chip architecture, and unlike cloud infrastructure businesses that require perpetual data centre investment, Hermès generates its margins by having extraordinarily skilled humans apply extraordinarily developed craft to extraordinarily scarce materials. The capex requirement is modest. The free cash flow conversion is among the highest of any large cap company on earth.

The Competitive Landscape Chanel

If forced to name a competitor to Hermès in the highest tier of leather goods and lifestyle luxury, one would name Chanel. No other house competes in the same psychological territory. Louis Vuitton is more accessible. Dior is more fashion forward. Prada is more intellectual. Gucci cycles through creative directors and aesthetic identities with unsettling regularity. Only Chanel shares with Hermès the quality of being a house whose mythology is larger than any individual product or season.

And yet Chanel is privately held by the Wertheimer family, meaning it is unavailable to public investors regardless of conviction. It also faces a different competitive dynamic: the classic flap bag and 2.55 have been dramatically inflated in price over the past decade in a deliberate strategy to chase Hermès positioning, but without the waiting list mechanics and without the same heritage in leather craft. Chanel's core identity is fashion and perfume. Hermès's core identity is the workshop.

The practical implication is that for a woman at the apex of global wealth who desires the ultimate expression of understated luxury in leather goods, there is functionally one answer. The Birkin is not a luxury product that competes with other luxury products. It is a category of one. The closest alternative is a Kelly bag, which is also made by Hermès. This is a competitive moat of remarkable purity.

LVMH

LVMH is the largest luxury conglomerate in the world by revenue, and Bernard Arnault is one of the most consequential business builders of the past half century. The case for LVMH as a long term holding is real. But it is a fundamentally different proposition from Hermès, and on a thirty year horizon the differences matter enormously.

LVMH's moat is width. Seventy five brands across wine and spirits, fashion and leather goods, perfumes and cosmetics, watches and jewellery, selective retailing. This diversification provides resilience: if one brand stumbles, others carry the portfolio. But it also creates dilution. The LVMH portfolio includes houses at every stage of the luxury lifecycle, from rising stars to brands in structural decline. Managing creative transitions across dozens of houses simultaneously is an execution challenge of extraordinary complexity.

The deeper issue is succession. Bernard Arnault is 76 years old. He has positioned five children across the group in senior roles, but a conglomerate of this complexity managed by family committee is genuinely uncertain territory. Hermès by contrast has legally fortified its ownership structure specifically to prevent the kind of hostile accumulation that Arnault himself attempted in 2010. When Arnault quietly acquired a 17 percent stake in Hermès through financial derivatives without disclosure, the Hermès family responded by creating a holding company, Emile Hermès SARL, that consolidated family shares with a voting agreement preventing dispersal. They essentially made themselves un-acquirable. That legal and structural architecture is itself a competitive advantage.

On a thirty year view: LVMH is a very good business. Hermès is a unique one.

Ferrari

Ferrari is the most intellectually honest comparison to Hermès because it shares the same fundamental logic: artificial scarcity of an aspirational product, extraordinary pricing power, a brand mythology that transcends product category, and a business model that produces exceptional margins by deliberately refusing to maximise volume.

Ferrari produces approximately 14,000 cars per year and has publicly committed to never increasing production beyond the level that keeps waiting lists intact. The parallels with Hermès are precise. And Ferrari has proven that this model works spectacularly in the modern era: revenue has compounded impressively, margins are exceptional, and the brand has successfully extended into merchandise, licensing, and experiences without diluting core desirability.

But Ferrari carries a risk that Hermès does not: technological disruption of the internal combustion engine. The electric vehicle revolution is not a marginal threat to Ferrari. It strikes at the sensory core of the Ferrari experience: the sound, the vibration, the mechanical drama of a high performance combustion engine at full throttle. Ferrari has developed hybrid powertrains and is investing in electric technology, but the electric Ferrari is a philosophically different object from a V12 Ferrari. Whether that transition preserves or diminishes the mythology is genuinely uncertain over a thirty year horizon.

A Birkin faces no equivalent existential question. The craft required to make it, the materials it uses, and the emotional transaction it represents are not threatened by any technology currently visible or plausibly imaginable. This is the decisive advantage Hermès holds over even its closest structural analogue.

NVIDIA and ASML

The technology companies that dominate current moat rankings are genuinely exceptional businesses. NVIDIA's CUDA platform is the de facto standard for AI training. ASML's EUV lithography machines are the only path to advanced chips below 5nm. These moats are real and formidable.

But they share a fundamental characteristic: their value is contingent on the continuation of a specific technological paradigm. NVIDIA's dominance depends on GPU based parallel computing remaining the architecture of choice for AI workloads. If neuromorphic computing, optical computing, or quantum approaches achieve commercial viability within thirty years, the CUDA moat could become a historical footnote. ASML's monopoly depends on silicon lithography remaining the dominant chip manufacturing approach. Alternative architectures, chiplet designs, or radical new materials science could change that equation.

These scenarios are not certainties. They are possibilities, and over thirty years, possibilities compound into meaningful probabilities. The investor in Hermès faces no equivalent scenario. The proposition that wealthy humans in 2056 will desire beautifully handcrafted leather goods made by skilled artisans using traditional techniques is not vulnerable to any technological development currently conceivable. It is, if anything, strengthened by them.

Wealth Creation and the Growing Addressable Market

The global wealthy population is growing faster than at any point in modern history. According to projections from multiple wealth research institutions, the number of ultra high net worth individuals globally is expected to roughly double over the next twenty to twenty five years, driven primarily by wealth creation in Asia, the Middle East, and continued compounding in Western markets. This matters enormously for Hermès in a way that it does not for most businesses.

Unlike a mass market company whose total addressable market is constrained by the global population, Hermès's addressable market is the global wealthy population, which is growing rapidly and from which Hermès currently captures a very small fraction. Every new billionaire created in Vietnam, Indonesia, Saudi Arabia, or India is a potential multi decade Hermès client. The brand's mythology is genuinely global: it requires no localisation, no cultural adaptation, no product modification. A Birkin means the same thing in Seoul, Lagos, and London.

As the wealthy population doubles, the supply of Birkins grows at 7 to 10 percent annually. This structural gap between demand growth and supply growth is not an accident or a temporary imbalance. It is the business model. And it means that the pricing power Hermès currently exercises will not merely be maintained over thirty years. It will almost certainly increase.

The Age of AI and the Paradox of Handcraft

We are entering an era of unprecedented automation. Artificial intelligence will replace cognitive labour at scale. Robotics will replace physical labour. The economic disruption of these transitions will be vast. But they will produce, as a cultural counterreaction, something that may be Hermès's greatest unexpected tailwind: a profound increase in the perceived value of things made entirely by human hands.

When everything of practical utility can be produced by machine at minimal cost, the irreplaceable nature of human craft becomes the ultimate luxury signal. A bag stitched by a single Hermès artisan who has trained for years, using techniques unchanged for generations, using materials that required another human's expertise to source and prepare, is not merely a functional object. It is a monument to human skill at a moment when human skill is being rapidly displaced from economic production.

This is not speculation. It is already observable in the premium placed on handmade goods across categories, from Japanese knives made by master bladesmiths to hand painted Italian ceramics to bespoke suits from Savile Row. As AI and robotics advance, this premium will grow, not shrink. Hermès, which has always positioned itself as the antithesis of industrialisation, is structurally positioned to benefit from the very forces that most businesses fear.

The Hermès Woman Has no Alternative

It is worth dwelling on the competitive reality at the very apex of women's luxury. A woman of serious wealth who wants the most coveted leather good in the world has one choice. She can wait for a Birkin or she can wait for a Kelly. Both are made by Hermès. There is no competitive product that occupies the same psychological territory. Chanel's flap bag is beautiful and desirable but it is not in the same conversation. No other house has produced a leather good that achieves the Birkin's combination of functional elegance, investment value, and social signalling.

This is a competitive position of extraordinary rarity. In most luxury categories there are three to five houses that a seriously wealthy consumer would consider. In this specific category there is one house. The absence of genuine competition at the apex is not marketing mythology. It is verifiable in secondary market pricing, in waiting list dynamics, and in the cultural references that appear across languages and geographies when the concept of ultimate luxury in leather goods is discussed.

That monopoly of desire at the apex of the market is the most durable moat in consumer goods. It has survived 187 years. The question for the investor is not whether it will survive the next thirty. The question is what price you are willing to pay to participate in it.

Risk Assessment

China: Real Risk, Not Existential

Approximately 40 percent of Hermès revenue derives from Asia, with China representing a substantial portion of that. The Chinese luxury consumer has been cautious in 2025 and early 2026, reflecting a combination of property market stress, reduced consumer confidence, and a government that has at various points expressed discomfort with visible displays of extreme wealth. This is a real risk and it explains a meaningful portion of the current P/E compression.

The thirty year investor should assess this risk through the correct lens. China's middle class and wealthy class are on a structural growth trajectory that temporary cyclical weakness does not alter. The property market correction is painful but not permanent. The government's ambivalence toward visible luxury consumption creates headline risk but does not prevent private acquisition. And if China were to become structurally hostile to luxury consumption, Hermès's geographical diversification, while less than ideal, would allow it to sustain the business while the Chinese market found its new equilibrium.

The Succession Question

Unlike LVMH, where succession is a genuine open question, Hermès has already navigated its most critical ownership transition. Axel Dumas, a sixth generation family member, serves as executive chairman. The family holding structure that controls the company has been legally reinforced to prevent hostile acquisition and to maintain alignment across family branches. The artisanal philosophy and the scarcity strategy are institutionally embedded, not dependent on a single visionary individual.

The Valuation Is Never Cheap

The most honest criticism of Hermès as an investment is that it is never conventionally cheap. A P/E of 38.7 is expensive by almost any standard applied to any other business. The case for paying that premium rests entirely on the belief that Hermès's earnings quality, growth trajectory, and moat durability justify a premium to normal valuation frameworks. Investors who are uncomfortable paying premium multiples for quality businesses will find Hermès perpetually unattractive, and they will never own it, and they will watch it compound for decades.

The relevant comparison is not Hermès at 38.7x earnings versus a market index at 20x. The relevant comparison is Hermès at 38.7x versus its own historical trading range of 33 to 75x. On that basis, the current entry point is among the most attractive of the past decade.

Conclusion

Hermès International is the most defensible large consumer business on earth. Its moat is rooted not in technology that can become obsolete, not in regulation that can be reformed, and not in network effects that can be disrupted by a better network, but in a permanent dimension of human desire that has been present in every civilisation in recorded history. The business model translates that desire into exceptional financial outcomes: 41 percent operating margins, near total free cash flow conversion, and pricing power that increases in direct proportion to global wealth creation.

The current P/E of 38.7 represents a 21 percent discount to the ten year median, one of the widest discounts in the company's modern history outside of acute market dislocations. The near term headwinds from China and currency translation are real. They are not structural.

On a thirty year horizon, the structural case is overwhelming. Global wealth will roughly double the addressable market. The age of AI and robotics will paradoxically increase the cultural value of human handcraft. There is no alternative at the apex of women's leather goods. The family ownership structure ensures the philosophy will not be compromised by short term commercial pressure. The Lindy Effect works in Hermès's favour with every year that passes.

The competition comparison resolves cleanly: Hermès is superior to LVMH in moat purity and ownership structure, superior to Ferrari in technological immunity, and superior to technology companies in moat durability across paradigm shifts. It is inferior to none in the specific characteristic that matters most for a thirty year hold: the certainty that the business will be relevant, growing, and dominant in its category three decades from now.

The case for Hermès at current prices is not that it is cheap. It is that it is the most durable business available at a meaningful discount to its own fair value. For investors with a genuine thirty year horizon, the question is not whether to own it. The question is whether to own enough of it.

Opmerkingen