Hedging Against AI and Robotics with Hermès

- Tung

- 19 feb

- 6 minuten om te lezen

Robotics and artificial intelligence will almost certainly reshape both blue- and white-collar labor. Repetitive physical work in logistics, manufacturing, and warehousing faces accelerating automation. Cognitive work in law, accounting, research, coding, design, is increasingly augmented by models that compress tasks once performed by entire teams. The result is not necessarily mass unemployment, but structural productivity gains, margin expansion, and labor compression across most sectors. In short: very few industries remain untouched. Yet positioning capital to capture that inevitability is far harder than it appears.

Betting on “AI” requires two correct predictions. First, identifying which sectors benefit most. Second, and more difficult, identifying which specific companies will execute best within those sectors. The dispersion between winners and losers during technological transitions is extreme. The internet was inevitable. But most early leaders did not endure. Yahoo and AOL once dominated the digital frontier. Today they are barely a part of the conversation. Technological inevitability does not guarantee investment inevitability.

Even within AI itself, the challenge compounds. Hardware, foundation models, robotics platforms, software integration layers. Each layer may create value, but competitive moats remain uncertain, as can be seen in the competitive capex landscape described earlier.

Picking long-term winners in frontier technology is notoriously difficult. Early dominance rarely guarantees structural permanence. The investment question, therefore, is not which AI company dominates, but which narrative benefits regardless of the outcome.

One such narrative: monetizing the status game. At the highest tier, durable hierarchy goods tend to share three traits: recognizable exclusivity, controlled access, and cultural continuity. Hermès has mastered each. Its supply is intentionally constrained, discounting nonexistent, and access selective. The customer base is concentrated at the upper end of the wealth spectrum. Operating margins exceed 40%, reflecting pricing power rather than scale efficiency. Its products are timeless rather than cyclical, and the business does not rely on labor abundance, volume growth, or technological advantage. It monetizes status hierarchy.

The analysis that follows argues why Hermès can serve as a structural hedge in an age of automation.

Luxury is a zero-sum game

Luxury is not a productivity business. Its value derives not from efficiency, cost structure, or technological sophistication, but from exclusion. Status is inherently relative. A Birkin bag is not valuable because it performs a function better than alternatives; it is valuable because access is restricted.

Hierarchy and status have been persistent features of human societies since the earliest civilizations. Across cultures and eras, access to scarce goods has served as a marker of social position. At its core, ultra-luxury operates within a social hierarchy, where value exists only in comparison to others. If everyone can obtain the same object, it loses its signaling power.

In that sense, luxury functions as a zero-sum hierarchy game: its value depends on differentiation, not abundance. This dynamic is deeply human, rooted in social structure rather than manufacturing capability. Technological advances may increase output and reduce costs, but they cannot eliminate hierarchy or automate relative status.

Constraint in an age of abundance

Most companies pursue growth through expansion. Hermès preserves value through restraint. Production growth is deliberately moderated, distribution tightly controlled, and discounting nonexistent. Access is regulated through waiting lists. The company does not seek to fully satisfy demand; it sustains a deliberate imbalance between supply and desire.

This is not inefficiency. It is engineered scarcity. By refusing to optimize for volume, Hermès protects its pricing power and reinforces brand authority, remaining structurally detached from the scale-driven dynamics that define most industries.

Wealth dispersion in a k-shaped economy Technological revolutions historically increase returns to capital before labor dynamics adjust. In early phases, productivity gains accrue disproportionately to asset owners, those holding equities, real estate, and businesses, while wage growth lags. The result is widening wealth dispersion. Hermès serves the segment most directly exposed to this dynamic. Its clientele sits at the upper end of the global wealth spectrum, individuals whose purchasing power correlates more with asset appreciation than wage income. This positioning differentiates Hermès from broader luxury conglomerates such as LVMH, which services a wider income distribution, including consumers whose demand is more cyclical and wage-dependent.

The Lindy effect

Founded in 1837, Hermès has operated through industrialization, global conflicts, monetary regime shifts, globalization, the rise of mass manufacturing, and the internet era.

This continuity reflects structural independence from specific technological regimes. Brands that endure across multiple paradigm shifts often derive resilience from the fact that they are not tied to any single technological cycle. The longer they persist, the more deeply they embed themselves in collective perception.

This contrasts with elite industrial luxury names such as Ferrari. Ferrari must continuously keep pace with advancing technology to preserve relevance. Hermès faces no such obligation. Its products are not defined by technological superiority but by symbolic continuity. A Birkin does not require technological reinvention to remain desirable. That distinction matters in an age of accelerating innovation. Businesses tied to technological performance must continuously defend their edge. Businesses tied to cultural scarcity defend identity instead.

Economics

Hermès generated €16.0 billion in revenue in 2025, representing growth of +8.9% at constant exchange rates. Growth moderated compared to prior years, but remained solid across regions.

The Leather Goods and Saddlery segment, arguably the category most directly tied to status signaling, grew +13.1% at constant exchange rates, materially outperforming other divisions. By contrast, Perfume & Beauty declined (-7.6%) and Watches slipped slightly (-1.5%). The data suggests that the core scarcity-driven category remains structurally strong, while more accessible or discretionary segments show pressure.

Geographically, Japan, the Americas, and Europe all delivered double-digit growth, while Asia ex-Japan grew more modestly. Revenue expansion remains demand-driven rather than volume-driven.

Recurring operating income reached €6.6 billion, translating into an operating margin of 41.0%. Gross margin exceeded 70%, underscoring pricing power. That level of margin is exceptional in global consumer industries and rare even among luxury peers. For context, mass apparel companies typically operate with gross margins in the 45–60% range, while premium brands often sit between 55–65%. Hermès’ gross margin exceeded 70% in 2025, placing it at the upper boundary of the luxury spectrum. The business is not leveraging cost-cutting, financial engineering, or aggressive expansion to generate profitability. The economics reflect controlled scarcity. Net income attributable to shareholders reached €4.52 billion.

Cash generation further supports the strength of the model. Operating cash flow reached €5.6 billion. After €1.16 billion in operating investments and lease repayments, adjusted free cash flow amounted to €3.88 billion. Cash conversion remains strong relative to reported earnings. Hermès generates substantial excess cash without aggressive store expansion or large-scale industrial spending.

The balance sheet remains exceptionally conservative. At year-end 2025, the company held a net cash position of €12.2 billion, against equity attributable to owners of €18.8 billion.

Debt levels are minimal. Financial borrowings due in more than one year amounted to €34 million, with no short-term financial debt outstanding. Including lease liabilities of €2,312 million alongside €34 million in borrowings brings total financial obligations to €2,346 million. Even on this more conservative basis, net cash remains close to €9.9 billion.

Total liabilities amount to €5,477 million, against total assets of €24,322 million, implying equity attributable to owners of approximately €18.8 billion. With net income of €4.52 billion, this results in a return on equity of roughly 24%, achieved with minimal financial leverage. These figures indicate strong liquidity, limited leverage, and a defensively structured balance sheet.

Risks and structural caveats

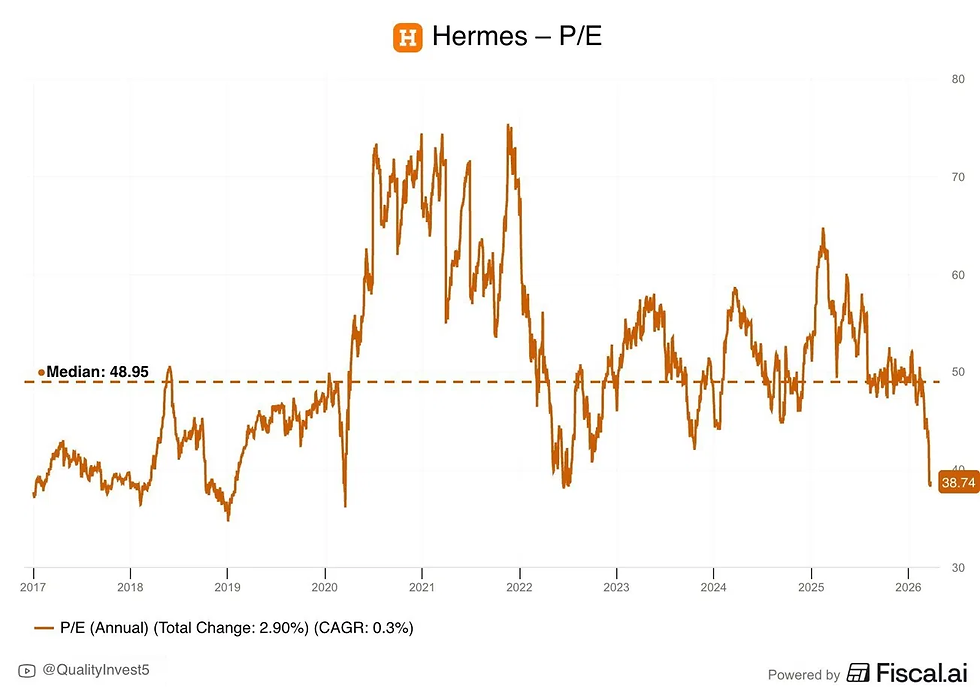

Hermès did not always trade at today’s elevated multiples. In the early 2000s, the company often traded between the high teens and mid-20s earnings range, consistent with how luxury was then perceived: largely cyclical and consumer-driven. As global wealth expanded, asset prices rose, and ultra-luxury brands proved resilient across crises, investors increasingly viewed Hermès less as a fashion house and more as a scarcity-driven franchise with durable pricing power.

However, luxury is ultimately driven by cultural relevance. If Hermès were to lose its aspirational appeal among future generations of wealthy consumers, growth could moderate regardless of its historical financial strength. Hierarchy and status signaling will most likely persist, but the brands representing it can shift over time.

Hermès benefits from geographic diversification, with revenue distributed across Asia, Europe, the Americas, and Japan. However, product concentration is more pronounced. Leather Goods and Saddlery represent the core economic engine of the business and account for a disproportionate share of growth and profitability. Categories such as perfumes, watches, and silk contribute to brand visibility but do not carry comparable margin weight. This means that the company’s financial profile remains closely tied to sustained demand for a relatively narrow set of ultra-luxury products.

Allocation Implications

Despite trading approximately 30% below its prior all-time high, Hermès continues to command a premium valuation. The shares trade at roughly 50x trailing earnings and in the low-40s on a forward basis. Within the luxury sector, large conglomerates such as LVMH or Kering typically trade in a 20–30x earnings range under normal conditions. Hermès has historically occupied the upper end of that range.

If broader market volatility compresses the multiple toward the high-30s earnings range while fundamentals remain intact, Hermès would present a more attractive opportunity to build a long-term position, particularly as a hedge against AI- and robotics-driven automation.

At current levels, however, much of the company’s structural strength is already reflected in the price, limiting scope for further multiple expansion. Future returns would therefore rely primarily on earnings growth rather than re-rating.

Opmerkingen